1.1.3. Python Random Generation

From Mathematical Distributions to Computational Samples

In Chapter 1.1, we established what probability means—whether as long-run frequencies or degrees of belief. In Chapter 1.2, we catalogued the probability distributions that model real phenomena—Normal, Exponential, Gamma, Poisson, and dozens more—understanding their mathematical properties, relationships, and when they arise naturally.

But theoretical understanding alone doesn’t generate data. When we need 10,000 bootstrap samples, a million Monte Carlo iterations, or posterior draws from an MCMC chain, we must bridge the gap from mathematical abstraction to computational reality. This chapter provides that bridge: a comprehensive guide to Python’s ecosystem for random number generation and probability computation.

Sampling from probability distributions underpins simulation, Bayesian inference, uncertainty quantification, and generative modeling. Python offers a rich ecosystem—from the zero-dependency standard library to high-performance scientific computing frameworks. Understanding when and how to use each tool is essential for effective computational statistics.

Road Map 🧭

Understand: How pseudo-random number generators create reproducible “randomness” and why explicit seeding matters for scientific work

Develop: Fluency with Python’s

randommodule, NumPy’sGeneratorAPI, and SciPy’sstatsdistribution objectsImplement: Sampling from all distributions covered in Chapter 1.2; weighted and stratified sampling; sequence operations

Evaluate: Performance trade-offs, parameterization conventions, and management of parallel random streams

The Python Ecosystem at a Glance

Before diving into details, here’s a map of the tools we’ll explore:

Category |

Library |

Why You Might Pick It |

Best For |

|---|---|---|---|

Standard Library |

|

Always available; quick scalar draws; simple shuffles; 11 classic distributions |

Teaching, prototyping, dependency-free scripts |

Scientific Computing |

|

Vectorized C/Fortran backends; 10–100× faster; array output; 50+ distributions |

Monte Carlo, bootstrap, large-scale simulation |

Statistical Modeling |

|

100+ distributions; PDF/CDF/PPF/fitting; statistical tests |

Distribution fitting, hypothesis testing, complete statistical toolkit |

Deep Learning |

|

GPU acceleration; differentiable distributions |

Neural network initialization, VAEs, reinforcement learning |

Probabilistic Programming |

PyMC, Pyro, Stan |

High-level model syntax; MCMC & VI engines |

Complex Bayesian models (covered in Chapter 5) |

The choice of library depends on your task. As a rule of thumb:

Need just a few random numbers? →

randommoduleNeed arrays of random numbers fast? → NumPy

GeneratorNeed probability calculations (PDF, CDF, quantiles)? →

scipy.statsBuilding a Bayesian model? → PyMC, Pyro, or Stan (Chapter 5)

Understanding Pseudo-Random Number Generation

Before using any library, we should understand what’s happening under the hood. Computers are deterministic machines—given the same input, they produce the same output. So how do they generate “random” numbers?

The Nature of Pseudo-Randomness

Pseudo-random number generators (PRNGs) are deterministic algorithms that produce sequences of numbers which, while entirely predictable given the algorithm and starting point, pass stringent statistical tests for randomness. When you call random.random(), you’re executing a mathematical formula that computes the next number in a deterministic sequence.

This determinism is actually a feature, not a bug:

Reproducibility: Given the same starting point (the seed), a PRNG produces exactly the same sequence. This enables scientific reproducibility—if you report bootstrap results, others can verify your exact computation.

Debugging: When a simulation produces unexpected results, fixing the seed lets you reproduce the problematic run while investigating.

Testing: Unit tests for stochastic code can have deterministic pass/fail criteria.

What Makes a Good PRNG?

A sequence \(u_1, u_2, u_3, \ldots\) behaves like independent draws from \(\text{Uniform}(0, 1)\) if it satisfies:

Uniformity: Values should be evenly distributed across \([0, 1)\). Dividing into \(k\) equal bins, each should contain approximately \(n/k\) of \(n\) total values.

Independence: Knowing \(u_t\) should provide no information about \(u_{t+1}\). No correlation between values at any lag.

Long period: The period—the length before the sequence repeats—should vastly exceed any practical simulation length.

High-dimensional equidistribution: When consecutive outputs are used as coordinates in high-dimensional space, points should fill the space uniformly.

Modern PRNGs are tested against extensive statistical test suites (like TestU01’s BigCrush). The generators in Python and NumPy pass these tests.

The Mersenne Twister

Python’s standard library uses the Mersenne Twister (MT19937), developed by Matsumoto and Nishimura in 1997:

Period: \(2^{19937} - 1\) (approximately \(10^{6001}\))—far exceeding any simulation need

623-dimensional equidistribution: Suitable for high-dimensional Monte Carlo

State size: 624 × 32-bit integers (19,968 bits)

Speed: Uses simple bit operations; very fast

Limitations: Not cryptographically secure (given 624 outputs, the state can be reconstructed). For security applications, use Python’s secrets module.

NumPy’s PCG64

NumPy’s modern Generator API defaults to PCG64 (Permuted Congruential Generator):

Period: \(2^{128}\) with smaller state (128 bits)

Better statistical properties: Passes even more stringent tests

Faster: Simpler operations on modern 64-bit CPUs

Jumpable: Can efficiently skip ahead, enabling parallel streams

For new projects, NumPy’s PCG64 is generally preferred over Mersenne Twister.

The Standard Library: random Module

The random module ships with every Python installation—no pip install required. It’s ideal for teaching, prototyping, and situations where external dependencies are problematic.

Generating Random Numbers

The foundation of all random generation is the uniform distribution on \([0, 1)\):

Function |

Output |

Notes |

|---|---|---|

|

|

Uniform on \([0, 1)\); the fundamental building block |

|

|

Uniform on \([a, b]\); implemented as |

|

|

Discrete uniform on \(\{a, a+1, \ldots, b\}\); inclusive on both ends |

|

|

Like |

Rule of thumb: Use random() for unit-interval floats; uniform(a, b) for self-documenting intervals; randint(a, b) for dice rolls and indices.

import random

from statistics import mean, pvariance

random.seed(42) # For reproducibility

# Generate U(0,1) samples

n = 1000

samples = [random.random() for _ in range(n)]

# Verify distributional properties

print(f"U(0,1) n={n}")

print(f" mean : {mean(samples):.5f} (theory 0.5000)")

print(f" variance : {pvariance(samples):.5f} (theory 0.0833)")

print(f" min…max : {min(samples):.5f} … {max(samples):.5f}")

Random Operations on Sequences

Beyond generating numbers, we often need to sample from existing sequences—selecting survey respondents, shuffling experimental treatments, or drawing cards.

Function |

Returns |

Replacement? |

Size |

Weights? |

When to Use |

|---|---|---|---|---|---|

|

One element |

— |

— |

No |

Pick a single winner, coin-flip between labels |

|

List of |

With |

|

Yes |

Bootstrap resampling, Monte Carlo from categorical |

|

List of |

Without |

|

No |

Deal cards, random subset for cross-validation |

|

|

— |

whole seq |

— |

In-place permutation (e.g., shuffle deck) |

Key distinction: choices (with replacement) allows duplicates; sample (without replacement) guarantees uniqueness. Bootstrap resampling uses choices; survey sampling uses sample.

import random

from collections import Counter

random.seed(42)

# choice: single random element

volunteers = ["Alice", "Bob", "Carol", "Deepak", "Eve"]

print(f"Today's volunteer: {random.choice(volunteers)}")

# choices: weighted sampling WITH replacement (loaded die)

faces = [1, 2, 3, 4, 5, 6]

weights = [0.05, 0.10, 0.15, 0.20, 0.25, 0.25] # Biased toward high values

rolls = random.choices(faces, weights=weights, k=10000)

print("\nLoaded die frequencies:")

for face, target_p in zip(faces, weights):

empirical_p = rolls.count(face) / len(rolls)

print(f" {face}: {empirical_p:.3f} (target {target_p:.2f})")

# sample: WITHOUT replacement (poker hand)

deck = [f"{r}{s}" for s in "♠♥♦♣" for r in "A23456789TJQK"]

hand = random.sample(deck, 5)

print(f"\nPoker hand: {hand}")

# shuffle: in-place randomization

items = list(range(10))

random.shuffle(items)

print(f"Shuffled: {items}")

Common Pitfall ⚠️

shuffle() works only on mutable sequences (lists). For strings or tuples, convert to a list first:

text = "HELLO"

letters = list(text)

random.shuffle(letters)

shuffled = ''.join(letters) # e.g., "OELHL"

Distribution Generators

The random module provides generators for common continuous distributions. Each uses the rate or scale parameterization noted below—pay attention to avoid errors.

Function |

Distribution |

Parameters & Notes |

|---|---|---|

|

Normal \(N(\mu, \sigma^2)\) |

Slightly faster than |

|

Normal \(N(\mu, \sigma^2)\) |

Thread-safe version |

|

Exponential with rate \(\lambda\) |

Mean = \(1/\lambda\). Not scale! |

|

Gamma with shape \(\alpha\), scale \(\beta\) |

Mean = \(\alpha \beta\) |

|

Beta(\(\alpha, \beta\)) |

Support \([0, 1]\); mean = \(\alpha/(\alpha+\beta)\) |

|

Log-Normal |

\(\exp(N(\mu, \sigma^2))\) |

|

Weibull with scale \(\alpha\), shape \(\beta\) |

Note: scale first, shape second |

|

Pareto Type I with shape \(\alpha\) |

Support \([1, \infty)\) |

|

Von Mises (circular normal) |

\(\mu\) = mean angle, \(\kappa\) = concentration |

|

Triangular |

Peak at |

import random

random.seed(42)

# Normal distribution

normal_samples = [random.gauss(0, 1) for _ in range(5)]

print(f"N(0,1): {[f'{x:.3f}' for x in normal_samples]}")

# Exponential - RATE parameter (mean = 1/rate)

# For mean = 2, use rate = 0.5

exp_samples = [random.expovariate(0.5) for _ in range(5)]

print(f"Exp(rate=0.5, mean=2): {[f'{x:.3f}' for x in exp_samples]}")

# Gamma distribution

gamma_samples = [random.gammavariate(2, 3) for _ in range(5)]

print(f"Gamma(α=2, β=3): {[f'{x:.3f}' for x in gamma_samples]}")

# Beta distribution

beta_samples = [random.betavariate(2, 5) for _ in range(5)]

print(f"Beta(2,5): {[f'{x:.3f}' for x in beta_samples]}")

Example 💡: Verifying Distribution Properties

Problem: Verify that samples from standard distributions match their theoretical moments.

Implementation:

import random

from statistics import mean, pvariance

from math import gamma as math_gamma

random.seed(42)

n = 10000

distributions = [

("Normal(0,1)", lambda: random.gauss(0, 1), 0, 1),

("Exponential(λ=1)", lambda: random.expovariate(1), 1, 1),

("Gamma(α=2, θ=3)", lambda: random.gammavariate(2, 3), 6, 18),

("Beta(2,5)", lambda: random.betavariate(2, 5), 2/7, (2*5)/(49*8)),

]

print(f"{'Distribution':<22} {'Sample μ':>10} {'Theory μ':>10} {'Sample σ²':>10} {'Theory σ²':>10}")

print("-" * 66)

for name, sampler, mu_th, var_th in distributions:

samples = [sampler() for _ in range(n)]

mu_emp = mean(samples)

var_emp = pvariance(samples)

print(f"{name:<22} {mu_emp:>10.4f} {mu_th:>10.4f} {var_emp:>10.4f} {var_th:>10.4f}")

Result: Sample moments closely match theoretical values, confirming correct implementation.

Controlling Randomness: Seeds and State

Reproducibility is essential for scientific computing. The random module provides three mechanisms:

Function |

Purpose |

Key Details |

|---|---|---|

|

Initialize the PRNG |

Same seed → identical sequence; |

|

Capture full internal state |

Returns ~6300-integer tuple (Mersenne Twister state) |

|

Restore captured state |

Resumes stream exactly where it left off |

|

Independent RNG object |

Keeps multiple deterministic streams without touching global |

Typical patterns:

Scenario |

Recommended Approach |

|---|---|

Intro demo / unit test |

Call |

Pause & resume long simulation |

|

Parallel simulations |

Create |

Temporary determinism |

Store state, run code, restore: |

import random

# Reproducibility demonstration

random.seed(42)

run1 = [random.random() for _ in range(5)]

random.seed(42) # Reset to same seed

run2 = [random.random() for _ in range(5)]

print(f"Run 1: {run1}")

print(f"Run 2: {run2}")

print(f"Identical: {run1 == run2}") # True

# State save/restore

random.seed(42)

_ = [random.random() for _ in range(100)] # Advance state

saved = random.getstate()

batch1 = [random.random() for _ in range(5)]

random.setstate(saved) # Restore

batch2 = [random.random() for _ in range(5)]

print(f"Batches match: {batch1 == batch2}") # True

NumPy: Fast Vectorized Random Sampling

For serious scientific computing—Monte Carlo simulations, bootstrap resampling, machine learning—NumPy’s random module is essential. It’s typically 50–100× faster than Python loops and provides far more distributions.

Why NumPy Is the Default for Scientific Work

Feature |

What It Buys You |

|---|---|

ndarray-native |

Draws arrive in the same structure you use for linear algebra, broadcasting, pandas I/O |

Vectorized C/Fortran core |

|

Modern Generator API |

Independent streams ( |

PCG64 PRNG |

Tiny state, period \(2^{128}\), passes BigCrush; spawns parallel streams safely |

Dozens of distributions |

Uniform to Dirichlet, plus multinomial, hypergeometric, log-series, … |

The Modern Generator API

NumPy provides two APIs: the legacy API (np.random.rand(), etc.) using global state, and the modern Generator API using explicit objects. Always use the modern API:

import numpy as np

# Create a Generator with specific seed

rng = np.random.default_rng(42)

# Generate arrays of random numbers

uniforms = rng.random(10) # 10 U(0,1) values

normals = rng.standard_normal(10) # 10 N(0,1) values

integers = rng.integers(1, 7, 10) # 10 dice rolls {1,2,3,4,5,6}

print(f"Uniforms: {uniforms[:5].round(4)}")

print(f"Normals: {normals[:5].round(4)}")

print(f"Integers: {integers}")

Why explicit generators are better:

No hidden global state: Different code sections don’t interfere

Clear reproducibility: Pass generators to functions explicitly

Parallel safety: Create independent streams for workers

Better algorithms: Default PCG64 beats Mersenne Twister

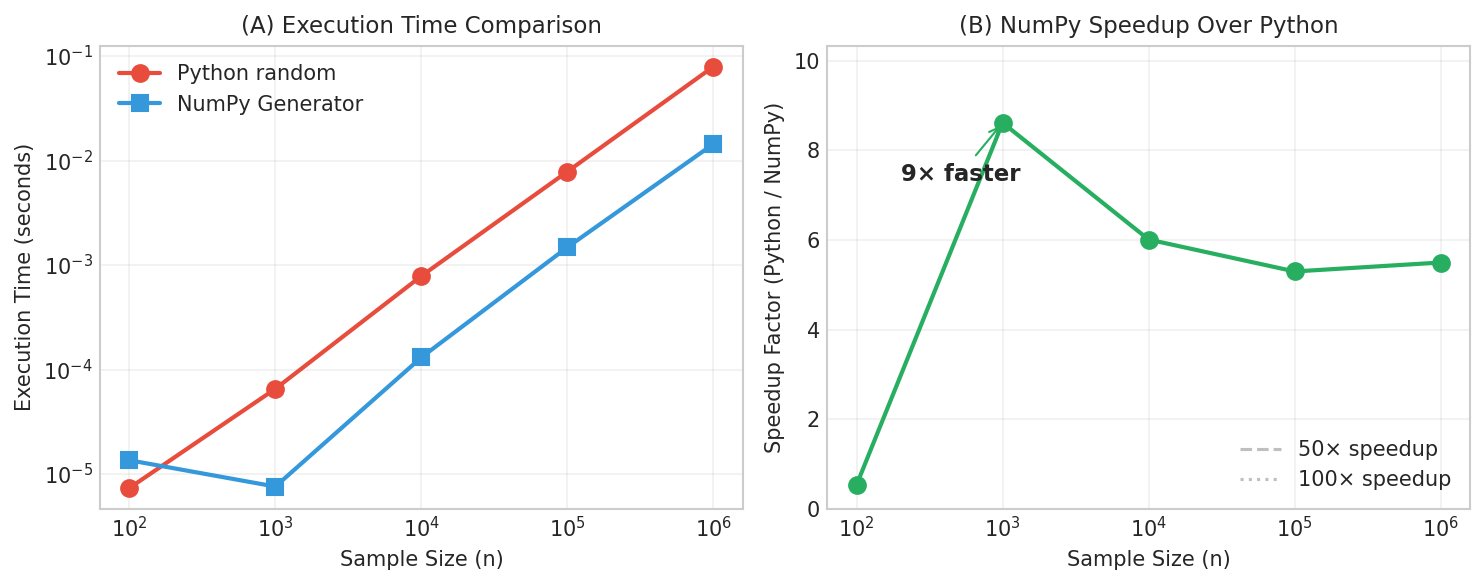

Performance Comparison

import random

import numpy as np

import time

n = 1_000_000

# Python standard library

random.seed(42)

start = time.perf_counter()

python_samples = [random.random() for _ in range(n)]

python_time = time.perf_counter() - start

# NumPy Generator

rng = np.random.default_rng(42)

start = time.perf_counter()

numpy_samples = rng.random(n)

numpy_time = time.perf_counter() - start

print(f"Python: {python_time:.4f} sec")

print(f"NumPy: {numpy_time:.4f} sec")

print(f"Speedup: {python_time/numpy_time:.1f}×")

# Typical: 50-100× speedup

Fig. 1.20 NumPy Performance Advantage. Speedups of 50–100× come from eliminating Python’s per-element overhead, not from faster random number algorithms.

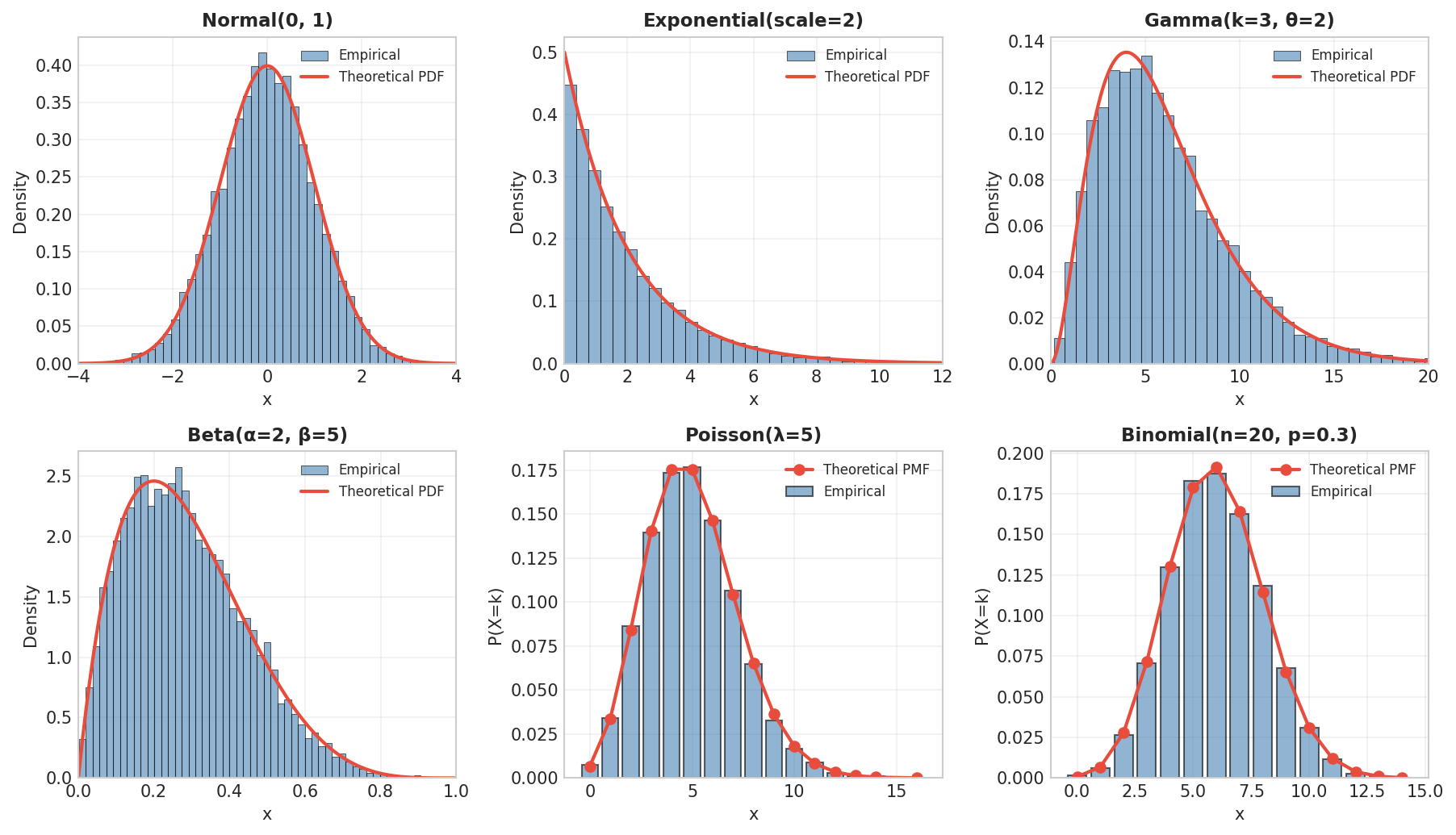

Univariate Distributions

NumPy provides generators for all distributions from Chapter 1.2:

import numpy as np

rng = np.random.default_rng(42)

n = 10000

# Continuous distributions

uniform_01 = rng.random(n) # U(0,1)

uniform_ab = rng.uniform(-3, 2, n) # U(-3, 2)

normal = rng.normal(loc=100, scale=15, size=n) # N(100, 225)

exponential = rng.exponential(scale=2, size=n) # Exp(scale=2), mean=2

gamma = rng.gamma(shape=2, scale=3, size=n) # Gamma(k=2, θ=3)

beta = rng.beta(a=2, b=5, size=n) # Beta(2, 5)

# Discrete distributions

binomial = rng.binomial(n=20, p=0.3, size=n) # Binom(20, 0.3)

poisson = rng.poisson(lam=5, size=n) # Poisson(λ=5)

geometric = rng.geometric(p=0.2, size=n) # Geom(p=0.2)

# Verify moments

print(f"N(100,15²): mean={normal.mean():.2f}, std={normal.std():.2f}")

print(f"Exp(θ=2): mean={exponential.mean():.3f}")

print(f"Gamma(2,3): mean={gamma.mean():.2f} (theory: 6)")

print(f"Poisson(5): mean={poisson.mean():.2f}, var={poisson.var():.2f}")

Fig. 1.21 Sampling from Common Distributions. Histograms of 10,000 samples with theoretical curves overlaid confirm correct implementation.

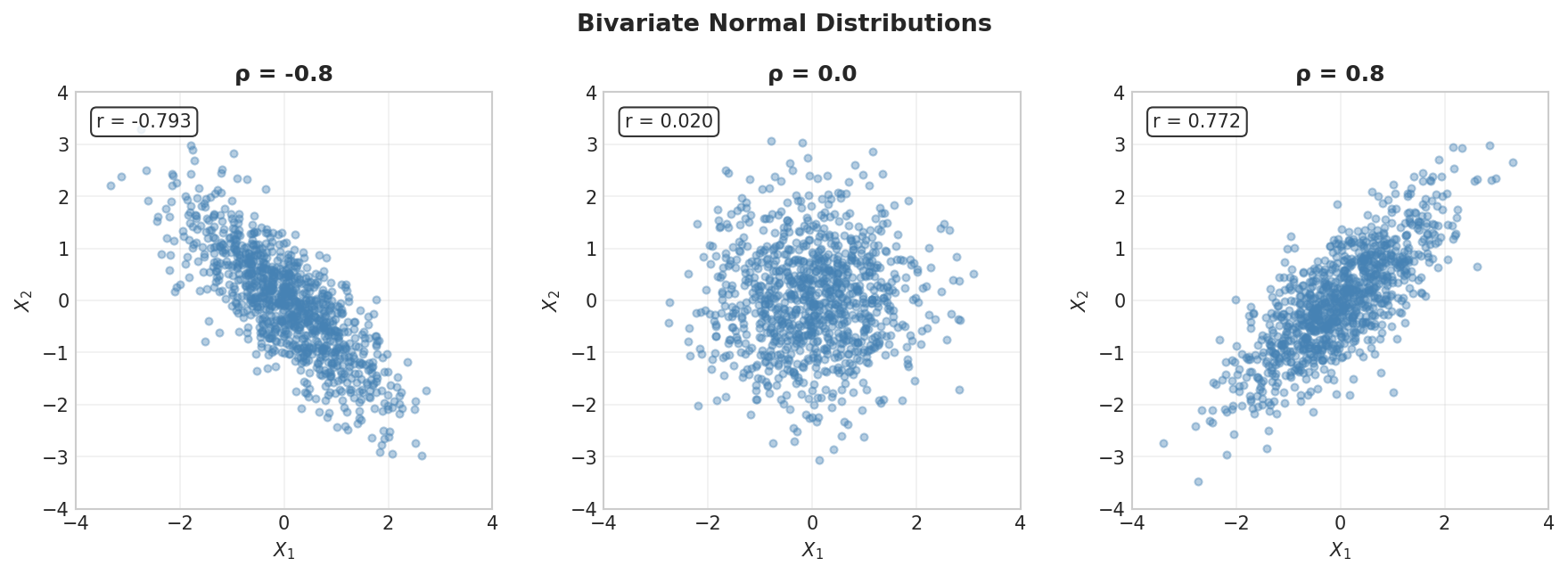

Multivariate Distributions

NumPy excels at multivariate distributions essential for modeling correlated data:

Multivariate Normal:

import numpy as np

rng = np.random.default_rng(42)

# Bivariate normal with correlation ρ = 0.8

mean = [0, 0]

cov = [[1.0, 0.8],

[0.8, 1.0]]

samples = rng.multivariate_normal(mean, cov, size=5000)

print(f"Sample correlation: {np.corrcoef(samples.T)[0,1]:.3f}")

print(f"Sample covariance:\n{np.cov(samples.T).round(3)}")

Fig. 1.22 Bivariate Normal with Different Correlations. Negative correlation creates downward-sloping clouds; positive correlation creates upward-sloping clouds.

Dirichlet Distribution:

The Dirichlet generates probability vectors (samples sum to 1)—essential as a prior for categorical data in Bayesian statistics:

import numpy as np

rng = np.random.default_rng(42)

# Dirichlet with concentration α = [2, 5, 3]

alpha = [2, 5, 3]

samples = rng.dirichlet(alpha, size=5)

print("Dirichlet samples (each row sums to 1):")

for i, s in enumerate(samples):

print(f" {i+1}: [{s[0]:.3f}, {s[1]:.3f}, {s[2]:.3f}], sum={s.sum():.6f}")

# Theoretical mean = α / sum(α)

print(f"\nTheory mean: {np.array(alpha)/sum(alpha)}")

NumPy Sampling Utilities

NumPy provides powerful functions for sampling from existing arrays:

Function |

Description |

|---|---|

|

Weighted sampling with/without replacement; axis-aware (NumPy ≥1.23) |

|

Return permuted copy along axis |

|

Shuffle in-place along axis |

|

Generate |

|

Random integers in |

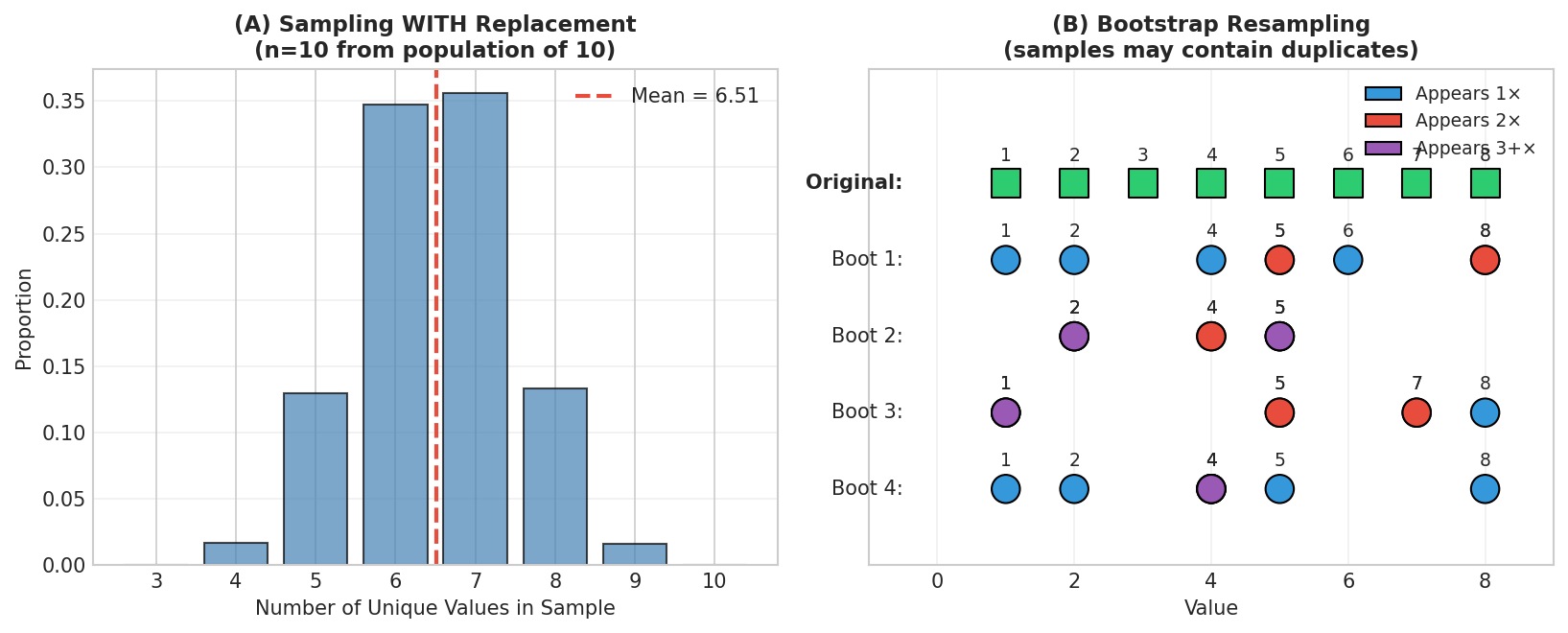

import numpy as np

rng = np.random.default_rng(42)

data = np.array([10, 20, 30, 40, 50])

# Sample WITH replacement (bootstrap)

bootstrap = rng.choice(data, size=10, replace=True)

print(f"Bootstrap sample: {bootstrap}")

# Sample WITHOUT replacement

subset = rng.choice(data, size=3, replace=False)

print(f"Unique subset: {subset}")

# Weighted sampling

weights = [0.1, 0.1, 0.1, 0.3, 0.4]

weighted = rng.choice(data, size=10, replace=True, p=weights)

print(f"Weighted (favors 40,50): {weighted}")

# Axis-aware bootstrap of rows

X = np.arange(15).reshape(5, 3)

boot_rows = rng.choice(X, size=5, replace=True, axis=0)

print(f"\nOriginal:\n{X}")

print(f"Bootstrap rows:\n{boot_rows}")

Fig. 1.23 Sampling With vs Without Replacement. Bootstrap resampling (with replacement) allows duplicates; simple random sampling (without) guarantees uniqueness.

Parallel Random Number Generation

For parallel computing, each worker needs an independent random stream. Naively using seeds 0, 1, 2, … doesn’t guarantee independence. NumPy’s SeedSequence provides the solution:

import numpy as np

from numpy.random import SeedSequence, default_rng

def mc_pi(child_seed, n_points=1_000_000):

"""Estimate π using one worker's independent stream."""

rng = default_rng(child_seed)

x, y = rng.random(n_points), rng.random(n_points)

return 4 * np.sum(x**2 + y**2 <= 1) / n_points

# Create master seed and spawn children

master = SeedSequence(42)

child_seeds = master.spawn(4)

# Each worker gets independent stream

estimates = [mc_pi(seed) for seed in child_seeds]

print(f"π estimates from 4 workers: {estimates}")

print(f"Mean: {np.mean(estimates):.6f}")

Common Pitfall ⚠️

Never share a Generator across threads or processes! Each parallel worker must have its own Generator from SeedSequence.spawn(). Sharing leads to:

Race conditions (undefined behavior)

Correlated streams (invalid statistics)

Non-reproducibility (results depend on timing)

SciPy Stats: The Complete Statistical Toolkit

While NumPy generates samples fast, scipy.stats provides the complete mathematical infrastructure: probability density functions, cumulative distributions, quantile functions, parameter fitting, and statistical tests.

Why SciPy Is the “Next Stop” After NumPy

Feature |

What It Buys You |

|---|---|

100+ distributions |

Gaussian to Zipf, each with PDF, CDF, PPF, RVS, fit |

Analytic functions |

Evaluate density, quantile, or survival at any point—no Monte Carlo noise |

Parameter fitting |

|

Hypothesis tests |

t-, Z-, KS-, Shapiro-Wilk, χ², Levene, Kruskal-Wallis, … |

Bootstrap helpers |

|

Decision cheat-sheet:

Task |

NumPy |

SciPy |

Go Beyond |

|---|---|---|---|

Vectorized random draws |

✅ |

— |

— |

Analytic PDF/CDF/quantile |

— |

✅ |

— |

Fit distribution parameters |

— |

✅ |

— |

Classical tests (t, KS, χ², ANOVA) |

— |

✅ |

— |

Linear/GLM/mixed models |

— |

— |

statsmodels |

Full Bayesian inference |

— |

— |

PyMC, Stan |

The Frozen Distribution Pattern

SciPy’s key design: create a distribution object with fixed parameters, then call methods on it:

from scipy import stats

# Create "frozen" distribution

iq_dist = stats.norm(loc=100, scale=15)

# Access properties

print(f"Mean: {iq_dist.mean()}")

print(f"Variance: {iq_dist.var()}")

print(f"Median: {iq_dist.median()}")

# Probability calculations

print(f"P(IQ ≤ 130) = {iq_dist.cdf(130):.4f}")

print(f"P(IQ > 130) = {iq_dist.sf(130):.4f}")

# Quantiles

print(f"90th percentile: {iq_dist.ppf(0.90):.2f}")

# Random samples

samples = iq_dist.rvs(size=5, random_state=42)

print(f"5 samples: {samples.round(1)}")

The Unified Interface

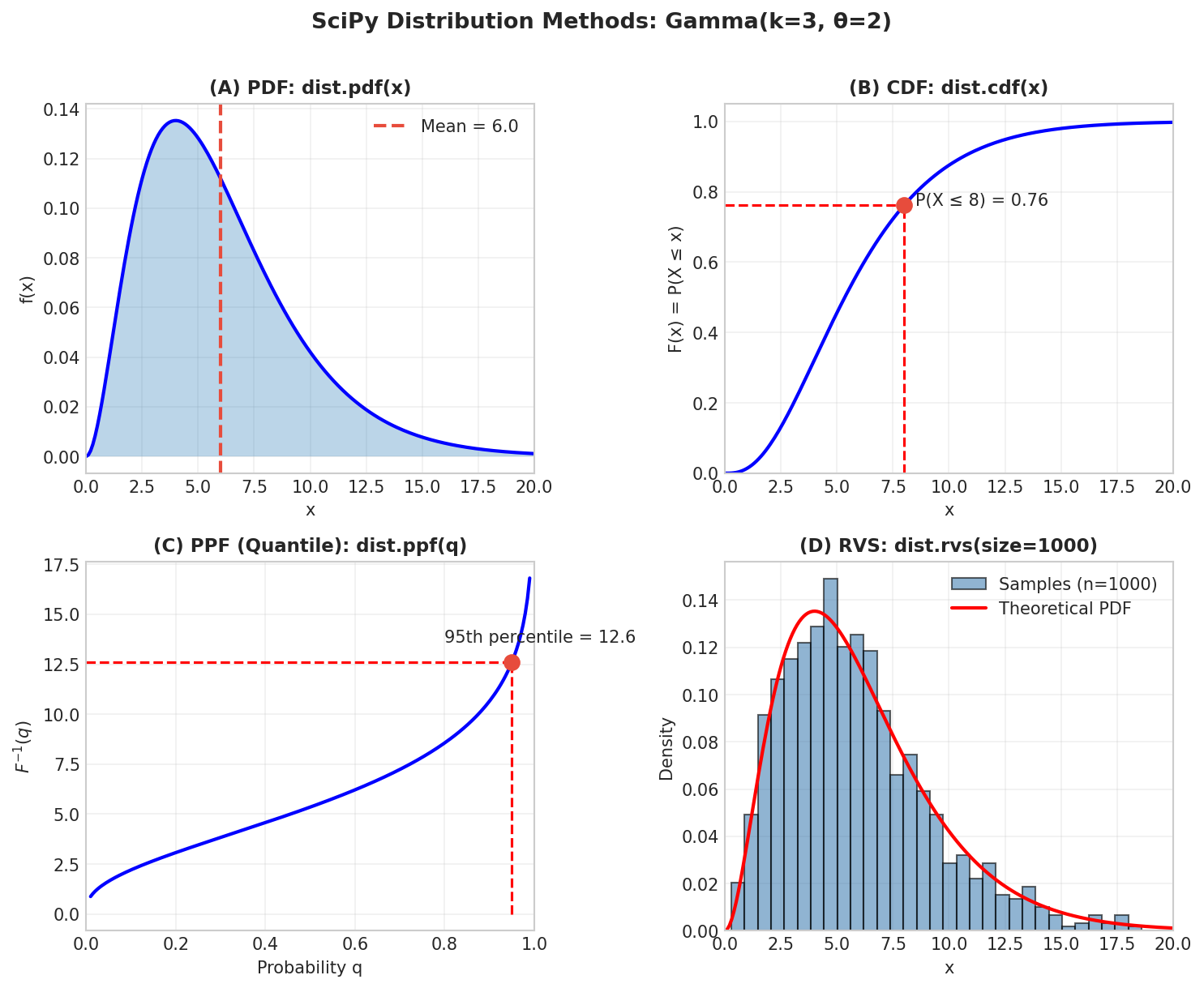

Every distribution provides the same methods:

Method |

Mathematical |

Description |

|---|---|---|

|

\(f(x)\) or \(P(X=x)\) |

Density (continuous) or mass (discrete) |

|

\(F(x) = P(X \leq x)\) |

Cumulative distribution function |

|

\(1 - F(x)\) |

Survival function |

|

\(F^{-1}(q)\) |

Quantile function (inverse CDF) |

|

— |

Random samples |

|

\(E[X]\), \(\text{Var}(X)\) |

Moments |

|

\([a,b]\): \(P(a \leq X \leq b) = \alpha\) |

Central probability interval |

|

\(\hat{\theta}_{\text{MLE}}\) |

Maximum likelihood estimation |

Fig. 1.24 SciPy Distribution Methods. (A) PDF gives density at any point. (B) CDF gives cumulative probability. (C) PPF (quantile function) inverts the CDF. (D) RVS generates samples matching the distribution.

Parameterization: The Most Common Error Source

Different sources use different parameterizations. SciPy has its own conventions:

Distribution |

SciPy Call |

Notes & Gotchas |

|---|---|---|

Normal |

|

|

Exponential |

|

Mean = scale = 1/rate. For rate λ=2, use |

Gamma |

|

|

Beta |

|

Shape parameters α, β |

Chi-square |

|

Degrees of freedom only |

Student’s t |

|

Add |

F |

|

Numerator df first |

Poisson |

|

|

Binomial |

|

n trials, probability p |

Negative Binomial |

|

Counts failures before n successes |

Common Pitfall ⚠️: Exponential Parameterization

The exponential distribution causes endless confusion:

Rate parameterization (textbooks): \(f(x) = \lambda e^{-\lambda x}\), mean = \(1/\lambda\)

Scale parameterization (SciPy/NumPy): \(f(x) = \frac{1}{\beta}e^{-x/\beta}\), mean = \(\beta\)

For mean = 2:

random.expovariate(0.5)— rate = 0.5rng.exponential(2)— scale = 2stats.expon(scale=2)— scale = 2

Always verify by checking the sample mean!

from scipy import stats

import numpy as np

# Want mean = 2

dist = stats.expon(scale=2) # Correct

samples = dist.rvs(10000, random_state=42)

print(f"Mean: {samples.mean():.3f}") # ≈ 2.0

# Common mistake

wrong = stats.expon(scale=0.5) # This has mean = 0.5!

Complete Analysis Example

Example 💡: Distribution Fitting and Diagnostics

Problem: Fit a Gamma distribution to data and assess the fit.

from scipy import stats

import numpy as np

# Generate "observed" data

rng = np.random.default_rng(42)

true_dist = stats.gamma(a=2, scale=2)

data = true_dist.rvs(1000, random_state=rng)

# Fit Gamma distribution (fix location at 0)

a_hat, loc_hat, scale_hat = stats.gamma.fit(data, floc=0)

print(f"Fitted: shape={a_hat:.3f}, scale={scale_hat:.3f}")

print(f"True: shape=2.000, scale=2.000")

# Create fitted distribution

fitted = stats.gamma(a=a_hat, loc=loc_hat, scale=scale_hat)

# Goodness-of-fit test

D, p_value = stats.kstest(data, fitted.cdf)

print(f"\nKS test: D={D:.4f}, p-value={p_value:.4f}")

# Theoretical vs empirical quantiles

print(f"\n95th percentile: fitted={fitted.ppf(0.95):.2f}, empirical={np.percentile(data, 95):.2f}")

Bringing It All Together: Library Selection Guide

Use ``random`` (standard library) when:

Zero dependencies required

Teaching probability concepts

Simple prototypes or scripts

Sample sizes under ~10,000

You need

choice,shuffle,sampleon lists

Use NumPy ``Generator`` when:

Working with arrays and matrices

Sample sizes exceed 10,000

Performance is critical

You need multivariate distributions

Parallel computing with independent streams

Use ``scipy.stats`` when:

You need PDF, CDF, or quantile functions

Fitting distributions to data

Performing statistical tests

Computing theoretical properties exactly

You need exotic distributions (100+ available)

Combine them:

from scipy import stats

import numpy as np

# SciPy for distribution definition and analysis

dist = stats.gamma(a=2, scale=3)

theoretical_mean = dist.mean()

critical_value = dist.ppf(0.95)

# NumPy for efficient sampling

rng = np.random.default_rng(42)

samples = rng.gamma(shape=2, scale=3, size=100000)

# Verify

print(f"Theory mean: {theoretical_mean}, Sample mean: {samples.mean():.4f}")

Key Takeaways 📝

Pseudo-randomness is deterministic: PRNGs produce sequences determined by their seed. Reproducibility requires explicit seeding.

Three libraries, three purposes: Standard library for simplicity; NumPy for performance with arrays; SciPy for complete distribution analysis.

Know your parameterizations: Rate vs scale causes endless bugs. Always verify sample means match expectations.

Vectorize for speed: NumPy provides 50–100× speedup by eliminating Python loop overhead.

Independent streams for parallel work: Use

SeedSequence.spawn(). Never share generators across threads/processes.Outcome alignment: This chapter directly supports Learning Outcome 1 (simulation techniques) and provides the computational foundation for all subsequent chapters.

Looking Ahead: From Random Numbers to Monte Carlo Methods

With Python’s random generation ecosystem mastered, we are ready to put these tools to work. The ability to draw samples from probability distributions is not merely a computational convenience—it is the engine that powers modern statistical inference.

In Chapter 2, we turn to Monte Carlo methods: using random sampling to solve problems that would be analytically intractable. The techniques you’ve learned here—generating uniforms, transforming to other distributions, managing random streams—become the building blocks for:

Monte Carlo integration: Estimating integrals via random sampling, essential when closed-form solutions don’t exist

The inverse CDF method: Transforming uniform samples to arbitrary distributions using quantile functions (

ppf)Rejection sampling: Generating samples from complex distributions by accepting/rejecting proposals

Variance reduction: Techniques like antithetic variates and control variates that improve Monte Carlo efficiency

The connection is direct: every Monte Carlo estimate begins with a call to a random number generator. The numpy.random.Generator you’ve learned to use will generate the uniform samples; the scipy.stats distributions will provide the CDFs and PDFs needed for transformations and density evaluation. Understanding the computational tools in this chapter is prerequisite to understanding why Monte Carlo methods work and how to implement them efficiently.

Consider the preview exercise on parallel Monte Carlo integration at the end of this chapter—it demonstrates exactly this bridge: spawning independent random streams, generating samples, and averaging to estimate an integral. Chapter 2 develops the theory behind why this works and when it fails.